The true story

From “normal” to mortgage-free in five moves

Every number in the book is real or modelled with transparent, checkable maths — the honest version, including what it actually took.

01

The purchase

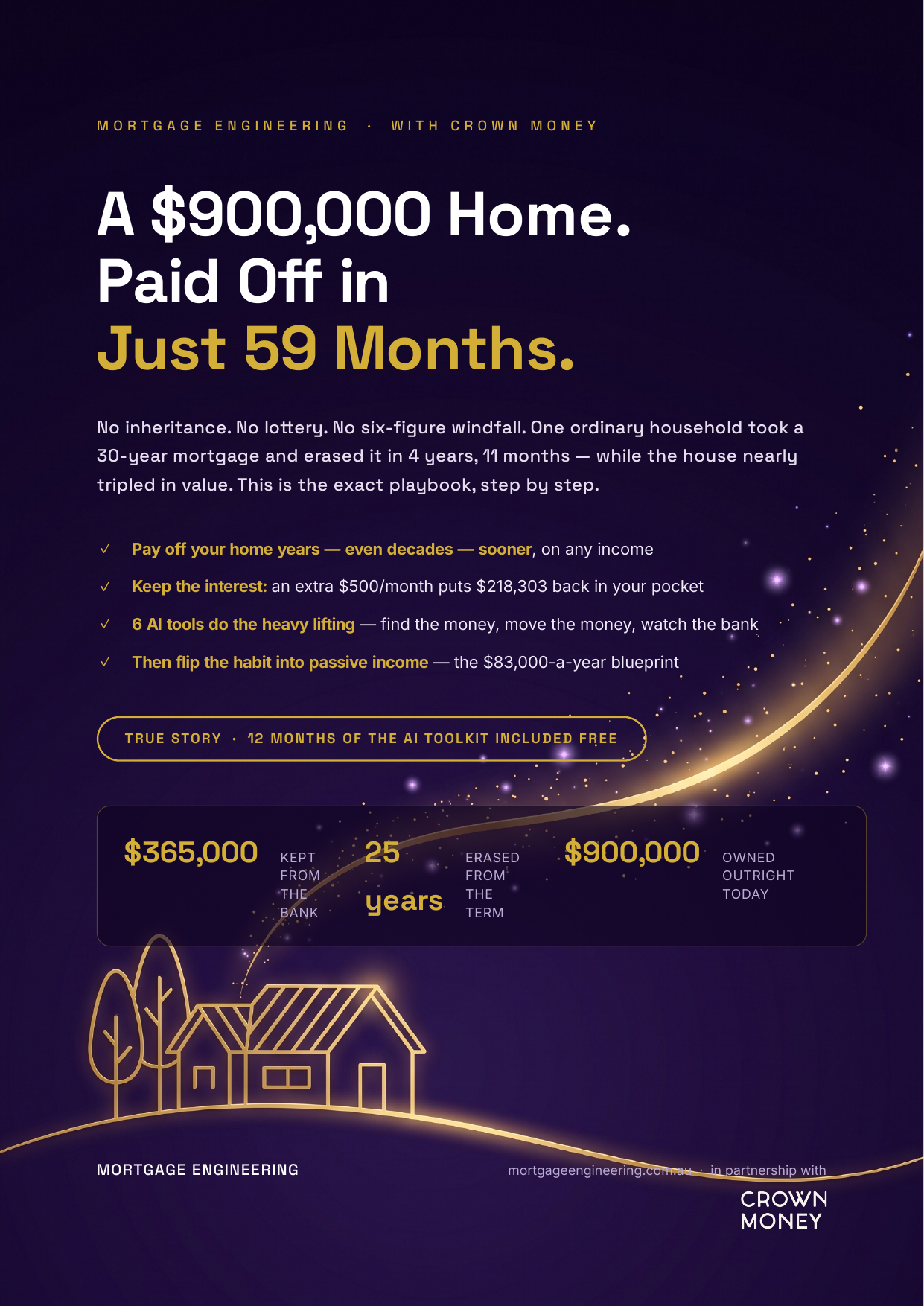

$325,000 property, $260,000 loan. An ordinary first home in an ordinary suburb.

02

Value rises

The bank approves a $105,000 equity redraw. Total owing: $365,000 — plus 30 years of interest to come.

03

The statement

One year of repayments, barely a dent. The spreadsheet says ~$422,809 of interest is coming. The rebuild begins.

04

The system

Five pillars deployed: AI audit, zero-touch automation, expense engineering, restructure, income expansion.

05

Month 59

Balance $0.00. Four years, eleven months. The house — worth $900,000 today — is 100% theirs.

“The bank had engineered the loan to maximise interest.

So we engineered our lives to minimise it.”

")

— Winner")